Your Comprehensive Guide to DORA Compliance: Essential Steps for European Fintech SMBs in 2025

The digital landscape for financial services is constantly evolving, and so is the regulatory environment. For CEOs and CTOs leading Small and Medium-sized Business (SMB) Fintech companies in Europe, staying ahead of compliance requirements is crucial for survival and growth. Enter the Digital Operational Resilience Act (DORA) – a significant EU regulation demanding robust digital defences across the financial sector.

Ignoring DORA isn’t an option, with the January 17, 2025, deadline fast approaching. But navigating its complexities can feel daunting, especially for resource-constrained SMBs. This comprehensive guide to DORA compliance is designed specifically for you. We’ll break down what DORA entails, why it’s critical for your Fintech SMB, and the key steps you need to take now.

What Exactly is DORA?

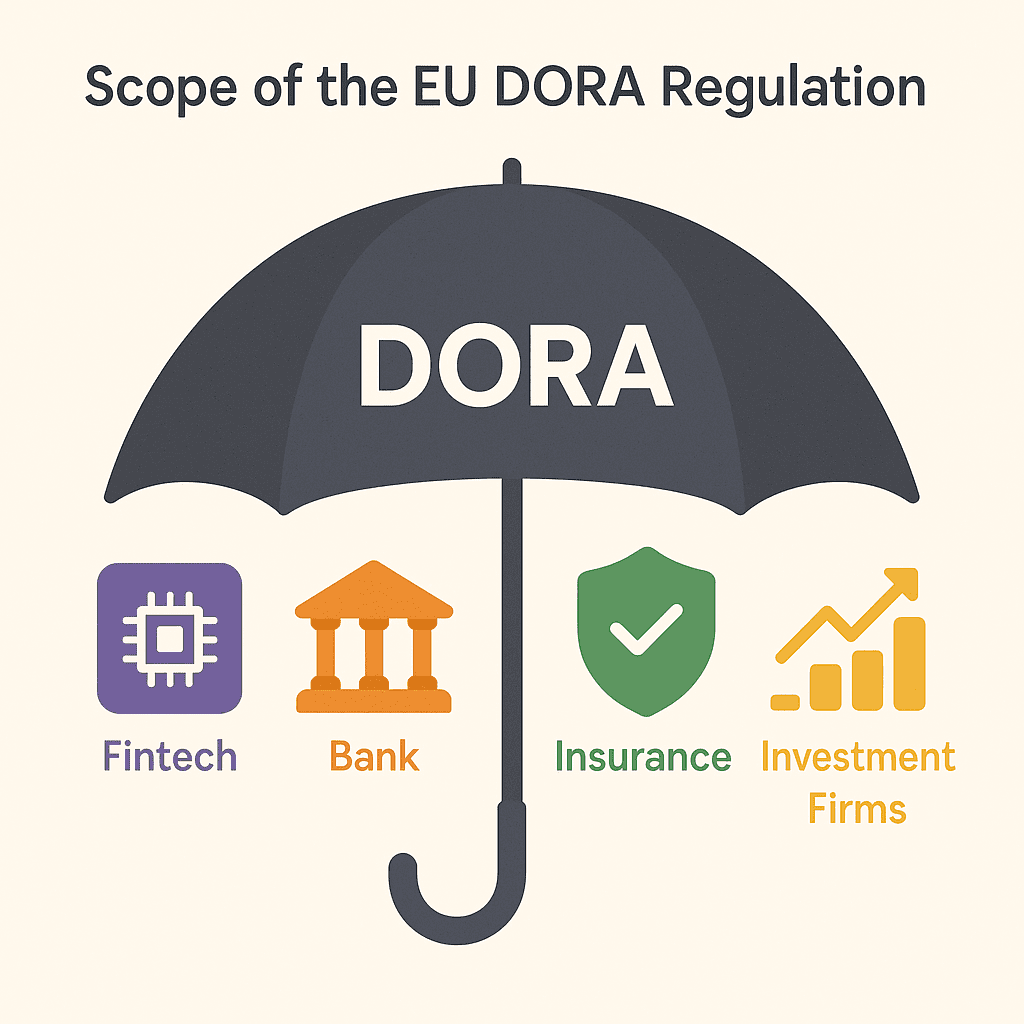

DORA (Regulation (EU) 2022/2554) is a binding EU regulation establishing a unified framework for digital operational resilience within the financial sector. Its primary goal is to ensure that all financial entities, including banks, insurance companies, investment firms, crypto-asset providers, and crucially, many Fintech companies, can withstand, respond to, and recover from all types of ICT (Information and Communication Technology) related disruptions and threats.

Think of it as a standardised digital immune system for the European financial ecosystem. It moves beyond fragmented national rules, creating a single set of requirements covering everything from cybersecurity preparedness to managing risks associated with third-party tech providers.

Why DORA is a Game-Changer for Fintech SMBs

While larger institutions might have dedicated compliance teams, DORA levels the playing field in terms of expectations. For Fintech SMBs, compliance presents both challenges and opportunities:

- Increased Scrutiny: Regulators will expect demonstrable resilience, regardless of company size.

- Third-Party Risk: Many Fintechs rely heavily on third-party ICT providers (cloud services, APIs, etc.). DORA places stringent requirements on managing these relationships.

- Competitive Advantage: Demonstrating DORA compliance can enhance trust with partners, investors, and customers, potentially becoming a competitive differentiator.

- Operational Stability: Implementing DORA principles inherently strengthens your business against cyber threats and operational failures, protecting your reputation and bottom line.

Failing to comply can lead to significant fines, operational restrictions, and reputational damage. Proactive engagement is key.

The 5 Key Pillars of DORA: A Breakdown for Leaders

DORA’s requirements are structured around five core pillars. Understanding these is the first step in creating your comprehensive guide to DORA compliance strategy:

1. ICT Risk Management

What it means: You need a comprehensive, well-documented ICT risk management framework. This isn’t just about firewalls; it covers governance, strategy, risk identification, protection and prevention, detection, response and recovery, business continuity, and continuous improvement. Action for SMBs:

- Conduct a thorough risk assessment, identifying critical ICT assets and potential threats.

- Develop and implement robust security policies and procedures.

- Ensure board and senior management oversight of ICT risks.

- Regularly review and update the framework.

2. ICT-Related Incident Management & Reporting

What it means: Establish processes to monitor, manage, classify, and report major ICT-related incidents to competent authorities using a standardised template. Action for SMBs:

- Define clear criteria for classifying incidents (especially “major” ones).

- Implement detection systems and response protocols.

- Designate clear responsibilities for incident management and reporting.

- Ensure timely reporting within DORA’s specified timeframes.

3. Digital Operational Resilience Testing

What it means: Regularly test your digital operational resilience capabilities to identify weaknesses and ensure preparedness. This includes vulnerability assessments, scenario-based testing, and, for critical entities, potentially advanced Threat-Led Penetration Testing (TLPT). Action for SMBs:

- Develop a risk-based testing program covering critical systems and functions.

- Schedule regular tests (e.g., annual vulnerability scans, periodic recovery tests).

- Document test results and implement remediation plans promptly.

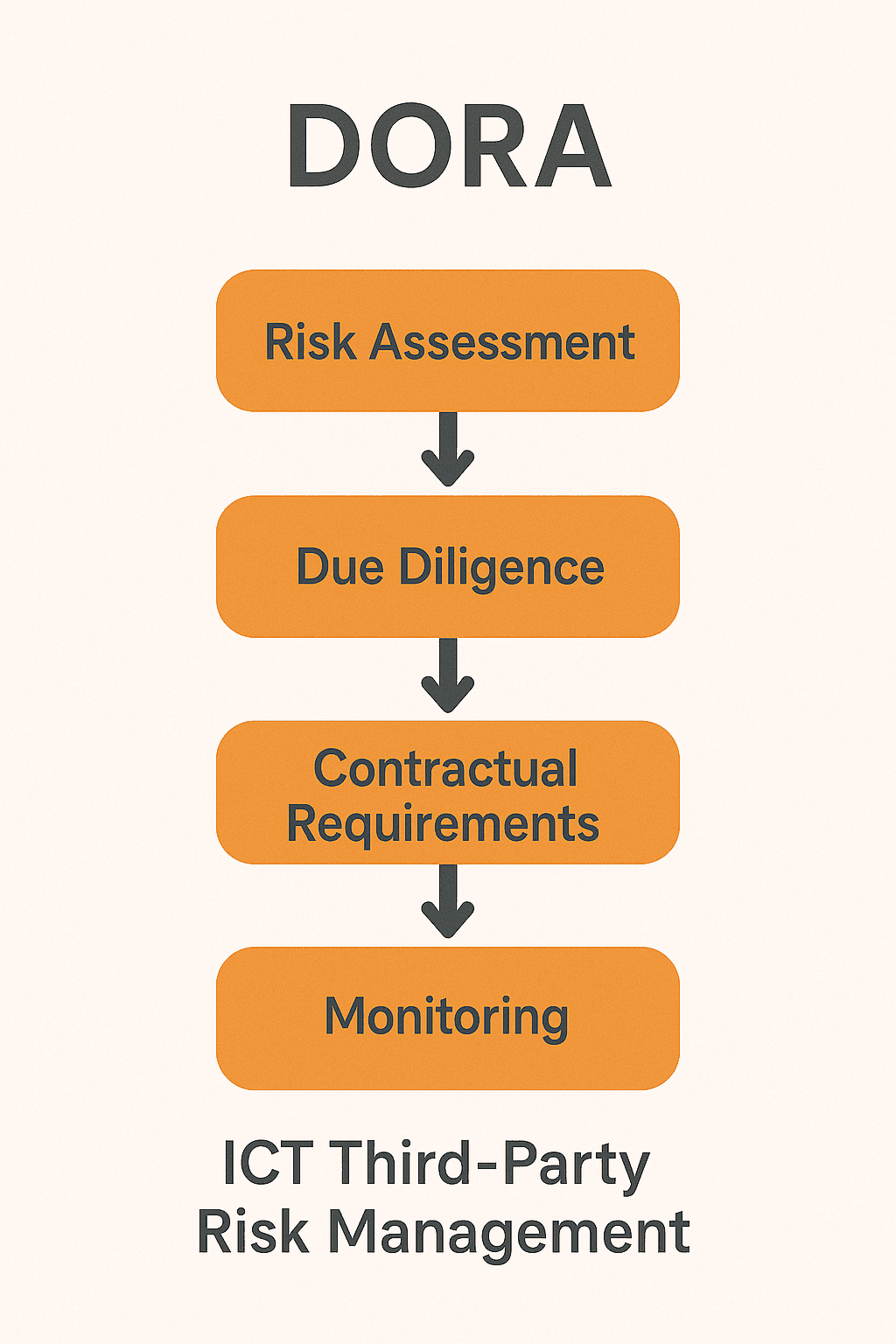

4. Managing ICT Third-Party Risk

What it means: This is vital for Fintechs. You must actively manage the risks associated with your ICT third-party providers (cloud, software, data analytics, etc.). This includes due diligence before onboarding, specific contractual requirements, ongoing monitoring, and exit strategies. Action for SMBs:

- Maintain a register of all ICT third-party service providers.

- Assess the criticality and risks associated with each provider.

- Ensure contracts include DORA-specific clauses (e.g., access/audit rights, security standards, exit support).

- Monitor provider performance and compliance.

5. Information Sharing Arrangements

What it means: DORA encourages (and in some contexts, requires) financial entities to exchange cyber threat intelligence and information amongst themselves to collectively strengthen resilience. Action for SMBs:

- Consider participating in relevant information-sharing communities or platforms (following security protocols).

- Establish internal processes for analysing and acting upon shared intelligence.

Your Roadmap to DORA Compliance: Getting Started

Feeling overwhelmed? Break it down into manageable steps:

- Assess Your Current State (Gap Analysis): Honestly evaluate your existing policies, procedures, and contracts against DORA’s five pillars. Where are the gaps?

- Develop a Remediation Plan: Prioritise the identified gaps based on risk and create a realistic timeline for addressing them. Assign ownership for each action item.

- Update/Create Documentation: Ensure your ICT risk management framework, incident response plans, BCP/DR plans, and third-party contracts are documented and DORA-aligned.

- Focus on Third-Party Providers: Review all ICT vendor contracts now. Start renegotiations if needed to include DORA requirements.

- Implement Testing: Schedule and begin conducting resilience tests appropriate for your risk profile.

- Train Your Team: Ensure relevant staff understand their roles and responsibilities under DORA, particularly regarding incident reporting and security practices.

- Seek Expertise: Don’t hesitate to engage external consultants or legal experts specialising in DORA if you lack internal resources.

The Cost of Inaction

Non-compliance with DORA by the January 2025 deadline carries significant risks:

- Substantial Fines: Regulators will have the power to impose hefty financial penalties.

- Reputational Damage: A security breach or operational failure post-deadline could severely damage customer trust.

- Operational Disruption: Regulators could impose measures restricting business activities.

- Loss of Partnerships: Partners may be unwilling to work with non-compliant Fintechs due to interconnected risks.

Conclusion: Build Resilience, Build Trust

DORA isn’t just another compliance checkbox; it’s a strategic imperative for European Fintech SMBs. By embedding digital operational resilience into your culture and operations, you meet regulatory requirements and build a more robust, trustworthy, and competitive business.

Use this comprehensive guide to DORA compliance as your starting point. The journey requires focus and resources, but proactive preparation is far less costly than facing the consequences of inaction. Start today to secure your Fintech’s future in the evolving European financial landscape.

Need help navigating your DORA compliance journey? Contact us today for a consultation.